Time to close your Branch? Recently we got a lot of enquiries whether clients need to go for POS, PDAs, Smartphones, Tablets, USSD or other, whether we have an app for Andoid or whether Loan Performer is web-enabled. Where to go? It’s confusion all over. Let’s try to clear the cloud!

Imagine you do not have a branch anymore, clients fill out their loan application via your website, you approve based on criteria that vary according to the loan amounts, disburse via mobile money and your clients repay via mobile money. Is that where we want to go? Is it even possible?

Though we are not a mobile money service provider, we can link up to one of them in your country and make mobile money disbursements and repayments possible. We have already done this for M-Cash in Uganda and in version 8.16 this is also possible for MTN, Airtel and UTL. We have linked up with Yo! Uganda which operates as an ‘aggregator’. An aggregator is an intermediary operator between the companies that need to receive payments, like National Water, Electricty etc and the mobile money providers. What is possible here in Uganda, is possible in any other country as well. You just need to bring us into contact with the local aggregator and we take it from there.

While currently the communication is via SMS messaging, we also anticipate USSD in future. Unlike SMS, which is store and forward based, USSD establishes a real time session between a mobile handset and an application handling service. So while with SMS evertime you send a message you have to wait for a reply, USSD is practically immediate. Another difference is that while the LPF SMS application depends on Java enabled phones, USSD works on all phones. The national communication commission issues what is called a “short code”, something like *999-99# that they issue to organisations like National Water etc The first 3 digits indicate the phone company and the next two indicate National Water etc. This will then show a menu on your phone where you can chose what you want to do. Another advantage is that whereas with SMS, messages can get lost, with USSD that is not possible.

We are currently in the process of implementing this in Kenya. Already Loan Performer can communicate with a USSD Gateway in this country and show client’s balances. We are now in the process of applying for a license from Safaricom so that we can integrate Loan Performer also with MPESA payments.

Now let’s have a look at the devices that help you bring your services closer to your clients. There is first of all the POS device. In the morning your credit officer can link the POS device to a workstation that is connected to the Loan Performer database. The person then downloads all savings and loan data for a particular group to the device and travels up-country. There, transactions are keyed in and the device can print a receipt for the client. At the end of the day the credit offericer returns, hooks up the device to the Loan Performer database and uploads the transactions of the day. Though POS devices can also be equiped with a mobile connection, they work especially well in areas where there is no reliable mobile network. In addition they are quite expensive (about 700$). Another disadvantage is that the credit officer has to travel with cash.

If a reliable mobile network is in place and if even mobile money agents are in the area, there is no need to send a credit officer to the field with a lot of money. The role of the credit officer changes and becomes more of a promotor or technical assistant who shows potential customers how easy they can transfer mobile money to their savings account or vice versa or make a loan repayment with mobile money. This is now by using a mobile phone, the Loan Performer app that sits on the phone and SMS Messaging or USSD.

With version 8.16 there will also be the possibility for the credit officer to enter a website, login into Loan Performer and enter transactions via a browser. If the client needs to get confirmation that a deposit has been received, you can enable the sending of SMS confirmations to the client’s phone once a transaction has been made on his/her account.

In addition with version 8.16 we can also provide a web-portal for clients or members of a Sacco where they can check their own shares, savings and loan accounts. We have decided to use a web interface rather than creating an app that only runs on an Android phone. For a web interface you can use any smartphone, tablet, laptop or computer and you are not limited to a specific operating system.

So lots of options to choose from. If you need any additional information let us know.

In this section our Technical Manager gives you some useful tips to make your life with Loan Performer more friendly.

The Windows User account has been deactivated or removed from the Domain.

Loan Performer 8.14 is able to automatically detect an available connection mode to the database. First it will check the availability of the domain and if the domain is not available, it will attempt to connect the database using a workgroup. If both of these channels are not available or not configured it returns the above message.

User does not have assigned access right(s) to the database.

Microsoft SQL Server maintains a security mechanism where users can not access database objects until access has been granted. Installing Loan Performer on a workstation does not necessarily mean the user has been granted access to the database Server (unless of course if the computer is the database server at the same time). In cases where the database is maintained on a separate computer the System Administrator has to explicitly grant access to new and existing windows account users (please do not assign ‘db_owner’ role to your users and the ‘public’ roleshould remain unchecked).

Connection to the database Server has been denied by a firewall on the Database server

In cases where one maintains a highly configured antivirus/firewall on the Database Server, connection to the database is established through specific ports. The system Administrator should maintain the SQL Server default Port 1433 and open or channel all database connections to a different open and secure port.

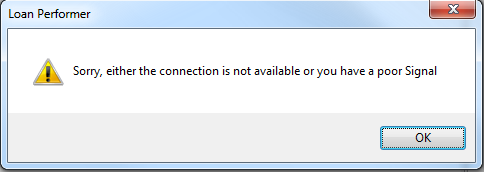

Virtual Private Network/Internet is down or poor

The above user message may be displayed by Loan Performer in cases where you are using Loan Performer on a Virtual Private Network or Internet. This simply means that you have a poor internet connection. The recommended bandwidth for Loan Performer is 1MBPS for both up- and downlink.

SMS is not working, LPF is not sending messages.

Client configured LPF to charge for SMS services and forgot to set the GL Account for SMS charges. LPF did not send messages because of that. And when SMS messages accumulated, the modem got overloaded. It kept sending but at a slow pace and kept freezing. Therefore, client is advised to configure the GL account for SMS charges and mark those old unsent messages as SENT to reduce the load on the modem and enable the server to start sending messages as they come.

The Versatitily of the Loan Application

The loan application screen is perhaps one of the most versatile features in the Loan Performer software. It’s been developed to accommodate almost all known loan application parameters/settings that users will ever want to use.

User-feedback has been instrumental in helping to enrich the loan application module. Most loan application settings were developed based on internationally-accepted best practices. The LPF application screen supports different loan products, installment types, interest calculation methods, grace periods, loan funds, interest payment methods etc. The feature also supports balloon loan payments, allows users to create repayment schedules with savings amounts to be paid with each installment either as a percentage or a flat amount, checks the availability of savings required to guarantee the loan, provides flexibility to calculate interest in days or months, etc. In this article, we can demonstrate just a few cases of a loan application with just few selected parameters.

Case 1

A loan of 100,000 USD at an annual interest rate of 36% per year for 8 months with a balloon repayment at the end and with interest on flat rate basis, will appears as follows:

The Loan Repayment schedule will appears as follows:

From the above schedule, you will notice that there are seven (7) interest-only installments plus one interest installment paid with the entire principal amount plus interest, making a total of eight (8) installments. Case 2

You can also consider a case of a loan of 100,000 USD at an annual interest rate of 36% per year for 6 months but with an upfront interest on a flat rate basis. Here LPF considers these settings as follows:

The repayment schedule generated shows that the first payment will only cover a small portion of principal payment and the entire interest payment while subsequent repayments will cover just the principal payments. Here the total paid at the end of each installment is equal for all installment dates as follows.

Case 3

In case of the lump sum upfront interest payment, the loan application settings appear as follows.

The Loan Repayment schedule appears as follows and all the interest for the entire loan term is paid with the first installment.

You may wish to note that just like in example 2, the total interest paid at the end of the loan term is the same (18,00 USD).

Case 4

In this example, we demonstrate a case where interest is deducted at disbursement. For a flat rate loan of 100,000 USD at an annual interest rate of 36% for 6 months but with interest deducted at disbursement, the settings are as follows:

The entire interest at the end of the loan term is realized at disbursement and only principal is paid during subsequent installments. In this case, the disbursement date is also the due date for interest payment. The repayment schedule is as follows:

LPF provides the user with many options to create different loan repayment schedules that suit his/her choice and probably this is one of the reasons that makes it the World’s number 1 microfinance software. We encourage you to explore various options that are available at the loan application screen.

LPF provides the user with many options to create different loan repayment schedules that suit his/her choice and probably this is one of the reasons that makes it the World’s number 1 microfinance software. We encourage you to explore various options that are available at the loan application screen.

Prepare for a Successful Implementation Implementing a Management Information System (MIS) is one of the most challenging initiatives a Microfinance Institution or Sacco can undertake. The better you are prepared, the more successful you will be!

A successful Loan Performer implementation will always depend on the characteristics of the Institution and its particular context in the market. However, having been in business for over 15 years, there is now much more experience in undertaking such implementations successfully and in our view there is a set of best practices that should be followed by Institutions in order to have a successful Loan Performer implementation done.

1. Prepare data in Excel Import templates provided with the installation of Loan Performer for importation. This is done by new clients who start working with Loan Performer. The preparation of the excel templates is to be done before data can be imported. However, we can assist if the client has difficulty in completing the excel templates. We can even validate the data to see whether it is done correctly.

2. Hardware/Computers should be well networked and necessary configurations done before starting work. For version 8 we recommend Pentium machines with 4 GB Ram. We also expect proper – non-pirated – operating systems in place. We have seen that in several places pirated operating systems gave us headaches to make our software work.

For a single branch, computers may have to be networked on a local area network (LAN) and a centralised database configured. For organisations having more than one branch, each branch may have a local area network with its own centralised database whereby at the end of a certain period, databases from different branches can be consolidated into one.

With version 8, Wide Area Network (WAN) Functionality makes it possible for institutions with several branches to have a centralised database. This allows clients to access their accounts from any branch.

This can be either with a single, centralised database or with syncronised databases, one for each branch. In the first case, you only need one IP address, in the second case each branch needs its own IP address. The 2nd option also requires a licensed SQL Server Database (not the Express edition).

3. Define clear business requirements/policies. Business policies in relation to Shares, Savings, Loans and Accounting should be ready before implementation. The client is required to have an operation's manual which spells out policies and procedures on how their business is run. It should bring out for instance fees to be charged, interest rate calculations methods for savings and loans, minimum and maximum loan amounts for loans, loan approval stages, procedures for data correction, backups etc. This is especially difficult for starting organisations who may not have these things in place.

4. Last but not the least, for clients upgrading from Version 7 to Version 8, we recommend refresher training for existing users upgrading from a lower to a higher version to help them understand new features that come with latest version.

When the above are fulfilled, a timely and successful Loan Performer implementation is assured. The Institution will improve its operations and increase its volume of business.

|

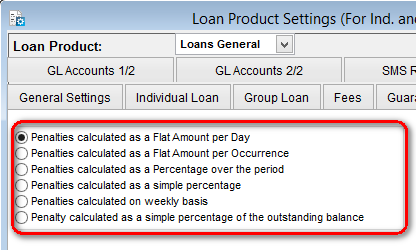

Penalty Calculation Methods In LPF We always get many questions about penalty calculations. Penalty calculations must be defined a loan product level, see menu “System/Configuration/Loan Product Settings”. Lets take you through the different options we have.

Loan Performer gives you six methods that you can use to calculate and charge penalties on bad loans. For each loan product, you have to define the penalty calculation method that will be applied when charging penalties at menu “Loans/Penalty on Arrears”.

1. Penalties calculated as a flat amount per day.

This method considers the number of days the loan is in arrears and the penalty is calculated as follows: Number of days in arrears x Penalty amount per day. Note that the amount to charge per day should be entered in the text box “Penalty amount per day” e.g., “2,000”.

2. Penalties calculated as a flat amount per occurrence.

If you choose this method, then each time you run the Penalties on Arrears module, the penalty charge set will be added to the client’s loan amount in arrears.

3. Penalties calculated as a percentage over the period.

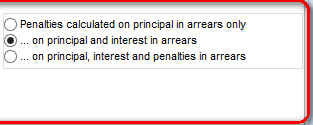

First of all, this method allows you to specify the components of the amount in arrears on which to charge the penalty. The organization can choose whether to charge penalty on the principal in arrears only, principal and interest in arrears only or the principal, interest and penalties in arrears. Two additional fields which allow you to specify the percentage and the minimum amount of penalty to consider appear (See the screenshot below):

The method considers the number of days that the loan is in arrears and the penalties are calculated as a percentage of the arrears for a given period. Amount in arrears x (Number of days in arrears/Number of days in a year) x Percentage.

4. Penalties calculated as a simple percentage.

This method does not consider how long the loan is in arrears but just calculates the penalty as at a given time as follows: Amount in arrears x Percentage.

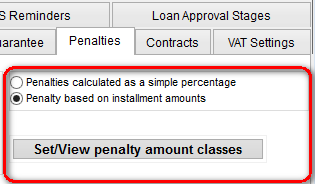

5. Penalties calculated on weekly basis

In this method penalties are calculated on a weekly basis as a simple percentage or based on the instalment amounts as shown below:

As a simple percentage, the penalties are calculated using the following formula: Amount in arrears x Percentage x Number of weeks in arrears.

If the penalty is to be calculated based on instalment amount, you have to specify the instalment amount classes and the charge to apply.

6. Penalties calculated as a simple percentage of the outstanding balance.

This method considers the outstanding balance and charges a fixed percentage at a given time. The penalty is calculated based on the following formula: Outstanding Balance x Percentage.

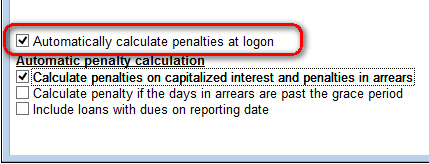

Note that you can set Loan Performer to automatically calculate penalties when starting the programme by ticking the “Automatically calculate penalties at logon” checkbox. This means that whenever you logon, LPF will automatically calculate penalties on qualifying loans and update the ledgers depending on the penalty calculation methods that you have defined above.

As an example, consider an organization that charges penalty as a flat amount per day. At configuration you have to set the penalty calculation method as “Penalties calculated as a Flat Amount per day” and you have to set the “Penalty amount per day” e.g., “2,000”. Then the configuration screen will look as follows.

To charge penalty you go to Loans->Charge penalty and set the necessary parameters on the following screen:

Click on the Calculate button to display the penalties that are due for the period:

The report on penalties charged will appear as follows;

If you are agree with the penalties calculated, click on the Yes button of the message dialogue box to book the amounts on the GL accounts defined on the other tabs of the window.

Note:

The user can set a limit on the period after which LPF stops calculating penalties for each of the above methods as shown below:

Loan Performer also allows you to delete loan penalties and other loan entries if need be. The user should go to Loans\Delete Loan Entries\Delete repayment\Penalty\Charge as shown in the figure below:

Loan Performer also has an audit trail which enables the person with the appropriate rights to trace who deleted a particular transaction such as a penalty charge at menu "System\Audit trail report".

Michel KITUNGWA LUMBU our Rep. in Congo

In this column we present to you different country representatives who can help you with training, implementation or support issues. This time we introduce one of our representatives in the Democratic Republic of the Congo, Michel KITUNGWA LUMBU. He is the Director in charge of Training and Implementation of Loan Performer at GEMIFIC.

Michel KITUNGWA LUMBU, our representative in the DRC

The Microfinance Expertise Group in Congo abbreviated as GEMIFIC (Groupe d’Expertise en Microfinance au Congo) got to know about the Loan Performer Software in 2004 through CARE, an International Development Corporation abbreviated as SOCODEVI – CARE (Société de Coopération de Développement International).

CARE had started two Savings and Loans Cooperatives in Kinshasa – DRC, Bomoko and Mufesakin. GEMFIC was hired to implement Loan Performer in the two cooperatives. Michael underwent training at Kinshasa conducted by Mr Hans Verkoijen in June 2004 and he underwent subsequent trainings in Uganda in 2006, 2009 and 2012. GEMIFIC began with Loan Performer version 6, they went to version 7 and now they are installing version 8.15 with all its new features.

Loan Performer is the most widely used Management Information System in majority of microfinance institutions in RDC and Congo Brazzaville due to its cost and constant improvement. GEMIFIC has trained and implemented Loan Performer at the Protestant University of Congo (l’Université Protestante du Congo – UPC) in RDC and in the following Microfinance institutions in RDC and Congo Brazzaville:

- Camec Kwilu Ngongo Savings and Loans Cooperative (August 2014)

- Mec IDECE Agence de Kimbaseke Savings and Loans Cooperative (April 2014)

- Union de Charité Savings and Loans Cooperative (May 2014)

- Mayombe Charité Savings and Loans Cooperative (October 2012)

- Crédit Populaire (CREP) Microfinance Institution (March 2012)

- 37 Microfinance Institutions in Congo Brazzaville (PARSEGD 2010 – 2011 Project)

- SODECCO Microfinance Institution at Pointe Noire Congo Brazzaville

- SMICO (March 2012)

- GALALETU, ADEKOR, COOPECDECOC Microfinance Institutions (PRESAR Project, December 2009)

- VIA NOVA Microfinance institution (June 2008)

- KALUDU Savings and Loans Cooperative (February 2008)

- MECRECO (2008)

- Lifevest Microfinance Institution (2008)

- MUCREFEKI and MUCREMBA Village Banks (2004-2006)

- BOMOKO and MUFESAKIN Village Banks (2004)

Michel Kitungwa can be contacted as follows:

Tel: +243-810523791, +243-970031664

Email: michelkitungwa@gmail.com

From the Loan Performer Users Community

| We welcomed the following Loan Performer Users: |

| |

- AAF, Aide Appui Financier, Burkina Faso

- Bura FSA, Kenya

- Camec Kwilu Ngongo, DRC

- ForevAfrica, Uganda

- Ngome FSA, Kenya

|

| We had the following trainings: |

| |

1.Loan Performer 8 for Power Microfinance, Uganda

|

| We had the following implementations: |

| |

1. The assistance to Visionfund Zambia has just ended and took 6 weeks..

2. The training and implementing of Loan Performer for Eclof Zambia was delayed and has just started.

3. We are training and implementing Loan Performer for Chibuku SACCOS in Botswana (and at the same time 2 new consultants).

4. We assisted Coocec Cahi, Paidek and Coocec Kivu in DRC Congo during 3 weeks on-site. |

| Other: |

| |

1. Robert Ombuya, One of our country representatives in Kenya finished training and implementation of Loan Performer for 2 FSA's on behalf of MESPT (Micro Enterprises Support Programme Trust). |

Next Training Opportunities We have every first Monday of the month a training session of 12 days (2 weeks, Monday to Saturday from 9:00 to 17:00 hrs) in Loan Performer version 8. Next training starts Monday 6 October 2014. This takes place at our office in Kampala. Costs are 750$ per participant. At the end of the training the participants have to pass a test and a certificate will be issued. Use this link to download the training schedule.

If Kampala is too far, we can do an e-training via the internet. The full training takes 12 sessions of 4 hours at a cost of USD 150 per session. We can also tune these trainings to your needs and make them more efficient for you.

We have started with an "EXPERT Training" in Loan Performer, targeting users of Loan Performer 8 who need to know all the ins and outs of this new version. It will be held on all 4 Saturdays during the month of September at our office. Upon request, the same can be done as an e-training. A training schedule is available here.

Need help with Loan Performer? Try the Online Help or Chat with our staff.

|